My wife and one of my closest friends told me that it is unethical to publish articles regarding the shares that I own because some readers who do not know me well would doubt my good intention. However, at my age and my financial standing I am not afraid to post this article as long as my intention is noble and altruistic. I want to teach you how to fish!

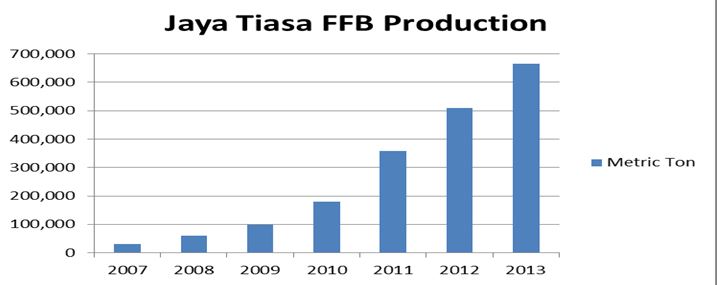

Since I wrote about Jaya Tiasa, many readers wanted to know about my other holdings. Mudajaya is my second largest holding. I also have some Xingquan, Success Transformer, Kulim, MFCB and smaller holdings of a few other counters.

As you know, many financial institutions are covering this stock and despite their frequent recommendations Mudajaya’s share price has been trading around this current level of Rm 2.70 in the last 3 or 4 years. Why should it be selling cheaper than its peers in terms of P/E ratio?

Mudajaya Price Chart

As you can see from the price chart, average price for the last few years is about Rm 2.70 and the downside risk is very small. For the share price to break out of this price range it needs a powerful catalyst which should be the announcement of its profit from its 26% share of the Independent Power Producer (IPP) concession in India. Let me give you a brief description of this project.

I was one of the original founders of Mudajaya and during my tenure, I constructed the 1st phase of the Tungku Jaffa power Station in Port Dickson about 40 years ago. Since then the company has completed 19 power plants as a construction contractor. The company specializes in power plant construction.

But in India, Mudajaya has taken a different role. Mudajaya holds 26% of a consortium to construct, own and operate 4 units of 360 Mega Watts coal fired power plant to generate electricity for sale to the Indian Government.

The total power is 4 units X 360 = 1440 mega watt. One mega watt can light up about 1,000 homes.

The estimated construction cost is about USD 4X360 MWX 1.3 million = USD 1.87 billion

The annual coal consumption is about 4,500 ton X 4X360 = 6,480,000 ton per year.

Assuming the coal price is USD 50 per ton, the annual cost of coal used = USD 324 million.

All these figures are mind boggling, hard to imagine any company has the financial ability to undertake this large concession for 25 years.

In India, a consortium of financial institutions finance the construction cost basing on the Power Purchase Agreement signed by the Indian Government. The banks must make sure that the power purchase agreement (the selling price of electricity) is profitable to Mudajaya and its partners otherwise the bank will not get back their money. The power purchase agreement is for 25 years and the power tariff will be adjusted to cover cost of coal, inflation, foreign exchange etc.

The first unit of 360 mw will be operational by end of March and the second unit will be operational by end of the 2ndquarter. By the end of the year all the 4 units will be in full operation.

The completion date has been postponed a few times until investors are fed up. As a result the share price remains depressed for so long. I believe the announcement of the additional profit spread over 25 years will be the catalyst to propel the price upward.

Today while I was writing this article, a big fund was buying aggressively to push the price up by 12 sens to close at Rm 2.80. The total volume traded was 2.972 million shares. It looks like the long delayed announcement of the additional profit from the Indian IPP concession will be out soon.

I am obliged to tell you that Mudajaya is my 2nd largest holding and I am not asking you to buy it. But if you do, I am not responsible for your losses.

Since I wrote about Jaya Tiasa, many readers wanted to know about my other holdings. Mudajaya is my second largest holding. I also have some Xingquan, Success Transformer, Kulim, MFCB and smaller holdings of a few other counters.

As you know, many financial institutions are covering this stock and despite their frequent recommendations Mudajaya’s share price has been trading around this current level of Rm 2.70 in the last 3 or 4 years. Why should it be selling cheaper than its peers in terms of P/E ratio?

Mudajaya Price Chart

As you can see from the price chart, average price for the last few years is about Rm 2.70 and the downside risk is very small. For the share price to break out of this price range it needs a powerful catalyst which should be the announcement of its profit from its 26% share of the Independent Power Producer (IPP) concession in India. Let me give you a brief description of this project.

I was one of the original founders of Mudajaya and during my tenure, I constructed the 1st phase of the Tungku Jaffa power Station in Port Dickson about 40 years ago. Since then the company has completed 19 power plants as a construction contractor. The company specializes in power plant construction.

But in India, Mudajaya has taken a different role. Mudajaya holds 26% of a consortium to construct, own and operate 4 units of 360 Mega Watts coal fired power plant to generate electricity for sale to the Indian Government.

The total power is 4 units X 360 = 1440 mega watt. One mega watt can light up about 1,000 homes.

The estimated construction cost is about USD 4X360 MWX 1.3 million = USD 1.87 billion

The annual coal consumption is about 4,500 ton X 4X360 = 6,480,000 ton per year.

Assuming the coal price is USD 50 per ton, the annual cost of coal used = USD 324 million.

All these figures are mind boggling, hard to imagine any company has the financial ability to undertake this large concession for 25 years.

In India, a consortium of financial institutions finance the construction cost basing on the Power Purchase Agreement signed by the Indian Government. The banks must make sure that the power purchase agreement (the selling price of electricity) is profitable to Mudajaya and its partners otherwise the bank will not get back their money. The power purchase agreement is for 25 years and the power tariff will be adjusted to cover cost of coal, inflation, foreign exchange etc.

The first unit of 360 mw will be operational by end of March and the second unit will be operational by end of the 2ndquarter. By the end of the year all the 4 units will be in full operation.

The completion date has been postponed a few times until investors are fed up. As a result the share price remains depressed for so long. I believe the announcement of the additional profit spread over 25 years will be the catalyst to propel the price upward.

Today while I was writing this article, a big fund was buying aggressively to push the price up by 12 sens to close at Rm 2.80. The total volume traded was 2.972 million shares. It looks like the long delayed announcement of the additional profit from the Indian IPP concession will be out soon.

I am obliged to tell you that Mudajaya is my 2nd largest holding and I am not asking you to buy it. But if you do, I am not responsible for your losses.